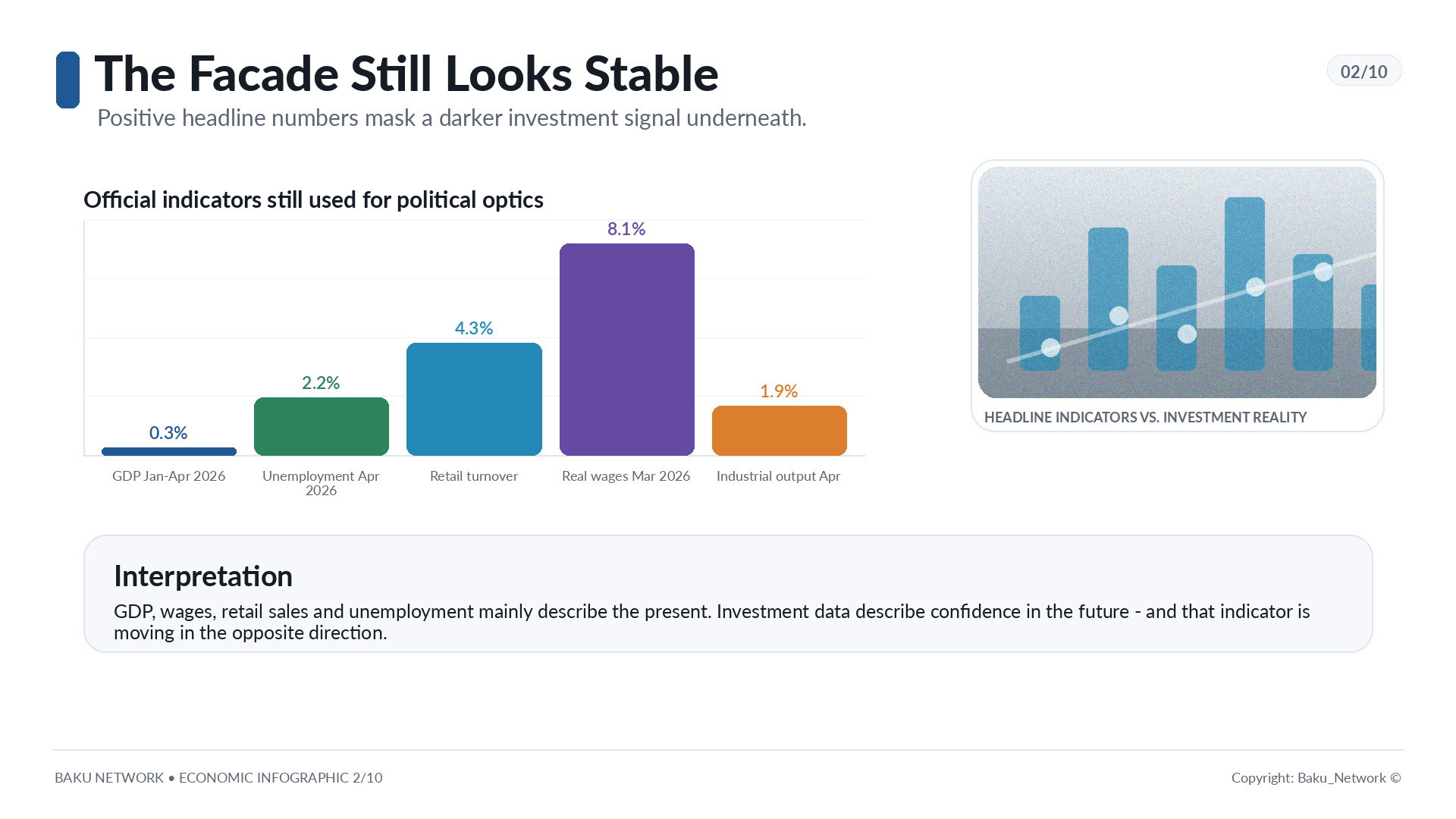

Outwardly, the Russian economy is still holding its posture. On paper, there is no collapse, no mass unemployment, no dramatic breakdown in consumption. Official statistics even retain figures that can be used to cover up the anxiety: in January–April 2026, GDP grew by 0.3 percent; unemployment in April remained at a historically low 2.2 percent; real disposable household income rose by 1.5 percent in the first quarter; retail turnover increased by 4.3 percent in January–April; real wages in March were 8.1 percent higher than a year earlier; industrial production in April added 1.9 percent.

For a political showcase, this is enough. For an economic diagnosis, it is not.

Russia’s main problem today is hidden not in current GDP, not in the employment rate, and not even in inflation. It lies deeper, in investment. In the money that businesses, the state, and corporations should be putting into buildings, structures, machinery, equipment, technologies, infrastructure, and future productivity. That is where the real crack begins.

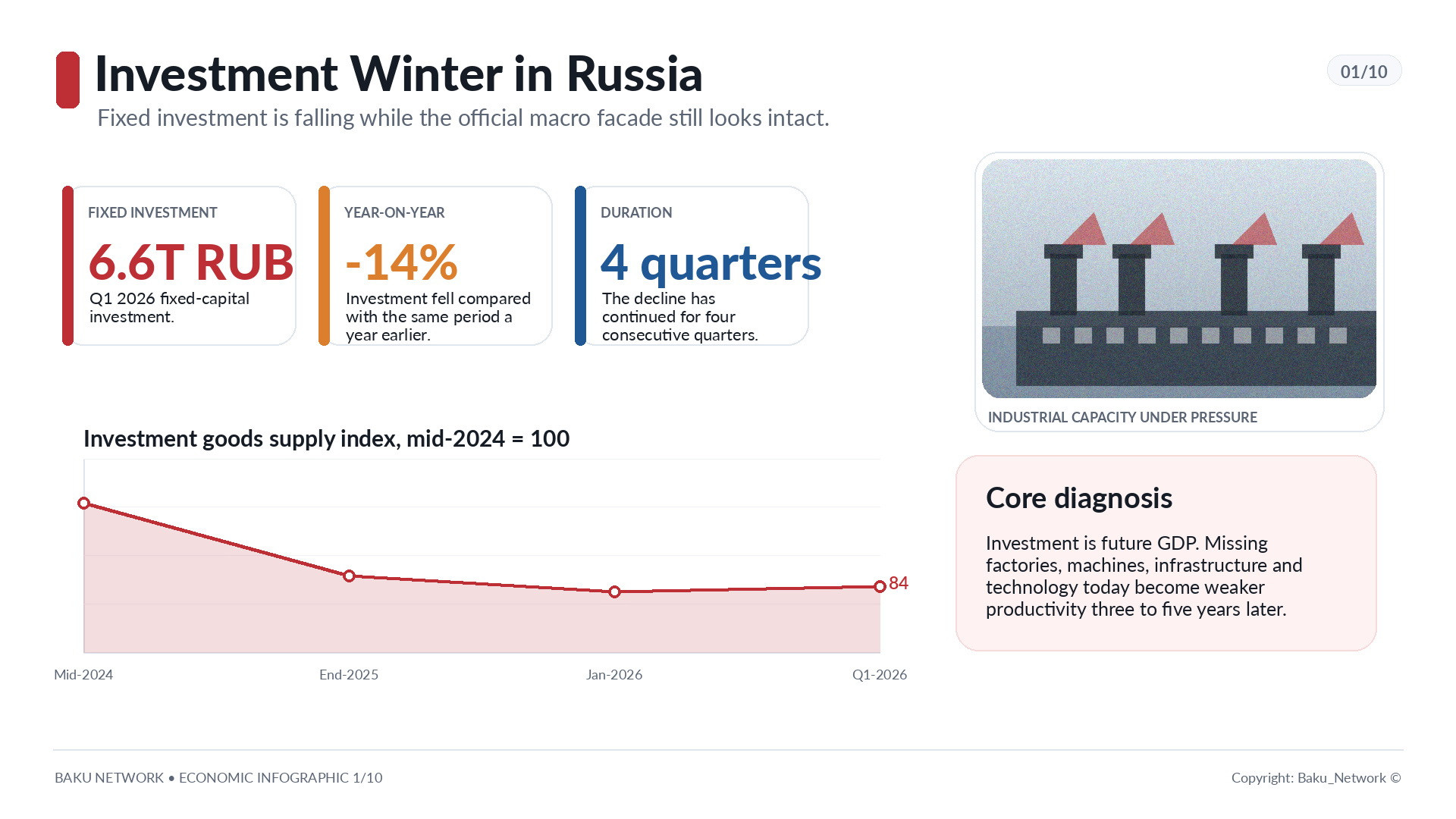

In January–March 2026, fixed capital investment in Russia amounted to 6.6 trillion rubles, 14 percent less than a year earlier. This is not random quarterly noise. The decline has continued for a fourth consecutive quarter. By the end of 2025, investment had fallen by 2.3 percent, entering negative territory for the first time since 2020. At the same time, not only the volume but also the quality of investment is deteriorating: the share of machinery and equipment has fallen to 34 percent. That means capital is working less and less for productivity and is increasingly flowing into less effective forms of maintaining the existing system.

Deputy Prime Minister Alexander Novak specified that the main part of the decline, 307 billion rubles, came from the largest companies, including Irkutsk Oil Company, Arctic LNG 2, and Gazprom. Against this background, only Rosneft increased investment, adding 18 billion rubles. But that does not change the overall signal: even big business, with access to state support channels, is beginning to cut long-term programs.

An economy can live for some time on old capacity. It can imitate normality through accumulated resources, the redistribution of budget flows, military orders, expensive consumer receipts, and extreme pressure on workers. But if new factories are not being built today, if modern machine tools are not being purchased, if infrastructure is not being renewed, then tomorrow the very foundation of growth disappears.

Investment is the GDP of the future. Its decline today means stagnation in three to five years.

A Country That Has Stopped Looking Toward Tomorrow

Ordinary macroeconomic statistics look backward, or at best capture the present. Inflation shows what has already become more expensive. GDP tells us what has already been produced. The key interest rate affects the economy with a lag, according to Bank of Russia estimates, from nine months to a year and a half. Investment works differently. It shows whether business believes in the future enough to risk money today.

A company does not build a plant for the next quarter. A railroad does not buy locomotives for the current report. An agricultural holding does not launch a new complex for a pretty presentation. All these decisions are made over a horizon of years. When investment falls, it means not merely that sentiment has worsened. It means economic agents are ceasing to plan expansion.

Other leading indicators confirm the same diagnosis. According to CMASF, the investment goods supply index in the first quarter of 2026 was 2.7 percent below the level of the fourth quarter of 2025. The January slump, which analysts linked to unusually cold and snowy weather in European Russia, was not offset in either February or March. The current level of investment activity is 16 percent below 2024 indicators and is already weaker even than the crisis months of 2022. Compared with the average monthly level of mid-2024, the supply of investment goods stood at 86 percent at the end of 2025 and 83 percent in January 2026.

The composite leading indicator for entry into recession reached 0.52 in February, with the critical threshold at 0.18. In March, it declined to 0.46, but still remained substantially above the danger line. The construction sector showed an attempted rebound in March, but CMASF analysts separately stressed that it was premature to speak of a recovery in housing demand or an improvement in the sector’s position.

The picture is unpleasant. Short-term indicators point to instability in the coming months. Investment points to risks over the coming years. Russia is entering not merely an investment pause, but a condition that increasingly resembles an investment winter.

Money Has Become Too Expensive

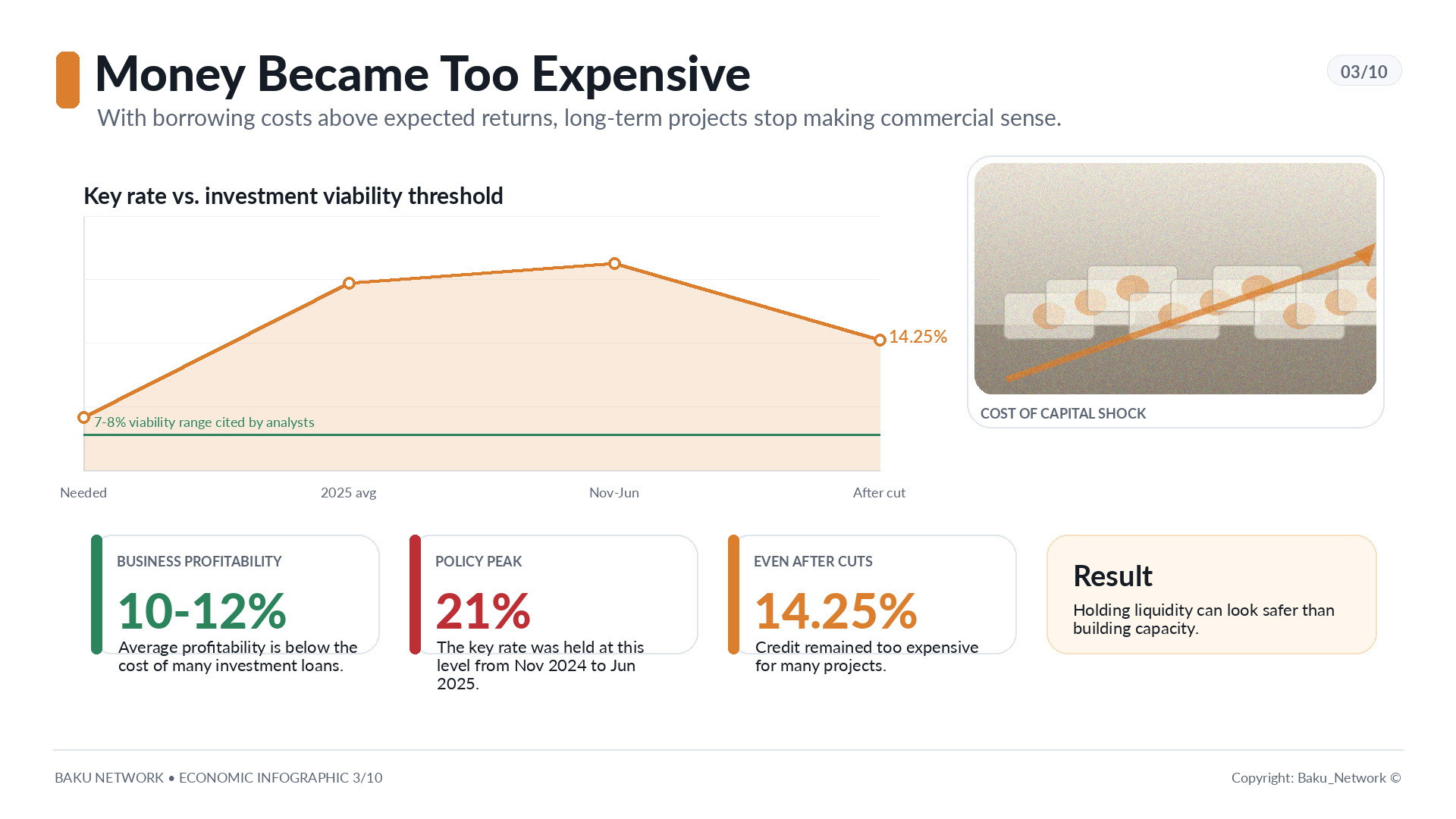

The first blow came from the cost of money. The private corporate investment cycle has effectively been frozen by the high key rate. From November 2024 through June 2025, the Bank of Russia held it at 21 percent; the annual average in 2025 was 19.27 percent. Even after the reduction to 14.25 percent, credit remained too expensive for most projects.

The average profitability of Russian business is 10 to 12 percent. With that arithmetic, borrowed funds cost more than the profit a project can generate. Expanding production with borrowed money becomes not entrepreneurship but financial self-punishment. Potential profit goes to interest payments, risks remain with the business, and the payback horizon grows murky.

Dmitry Belousov, deputy director of CMASF, precisely formulated the logic of this new caution: investment projects become economically meaningful at a rate of 7 to 8 percent. For now, it is easier and safer to keep money in accounts or in federal loan bonds than to enter projects whose payback is unclear.

The high rate hits twice. It makes loans expensive and simultaneously turns passive cash storage into a rational strategy. There is no need to build a workshop, buy equipment, look for engineers, argue with officials, depend on supplies, and live under the threat of a prosecutorial lawsuit. It is enough to place funds in financial instruments and wait.

Alexander Shokhin, head of the Russian Union of Industrialists and Entrepreneurs, listed the factors that cannot support long-term investment: a high interest rate, a strong ruble, high taxes, and uncertainty over property rights. Pavel Titov, president of Abrau-Durso, warned back in 2025 that such monetary policy did not imply serious investment. Even a retail investor chooses a bank deposit under these conditions. Big business chooses caution all the more.

Small Business Is No Longer Developing. It Is Surviving

Large companies at least have partial access to subsidized loans, project financing through VEB.RF, and state resources. Small and medium-sized businesses have found themselves in a different reality.

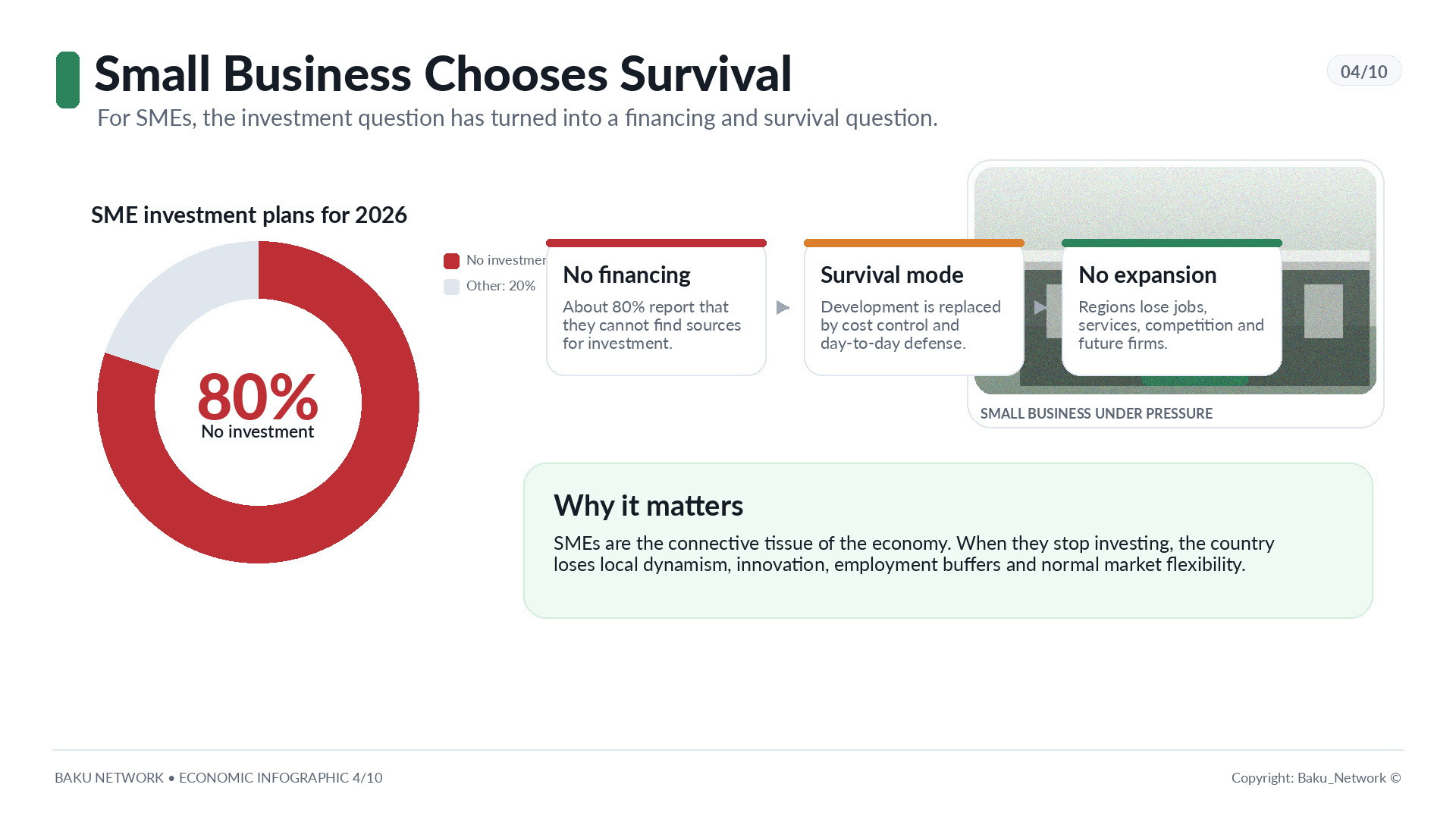

According to a survey by Opora Russia among 6,600 representatives of small and medium-sized enterprises, about 80 percent do not plan to invest in 2026 because they cannot find sources of financing. The organization’s head, Alexander Kalinin, put it bluntly: for many, the issue now is not development but survival.

This matters more than it may seem. Small and medium-sized business is not just a statistical category. It is the layer of the economy that creates employment, services, local competition, regional activity, and market flexibility. When it abandons development, the country loses not only future enterprises, but also the very fabric of normal economic life.

Bank of Russia surveys show that after economic uncertainty, the main factor obstructing investment is expected demand. The Central Bank’s latest enterprise monitoring recorded a decline in investment activity in the first quarter of 2026 to the average levels of early 2022. For the second quarter of 2026, the lowest investment growth since the fourth quarter of 2019 was expected.

Research by the Institute of Economic Forecasting of the Russian Academy of Sciences adds an important detail: for 40 percent of industrial respondents, capital expenditure planning does not depend directly on the level of the interest rate. The main obstacles are macroeconomic uncertainty and the lack of necessary equipment. Behind this formula lies not only expensive credit. There are sanctions, technological ruptures, the inability to legally buy or pay for machine tools, the risk of new taxes, fear of reduced state orders, and the threat of nationalization.

In a normal economy, an entrepreneur fears a market mistake. In today’s Russian economy, he increasingly fears the state.

Nationalization as Economic Cold

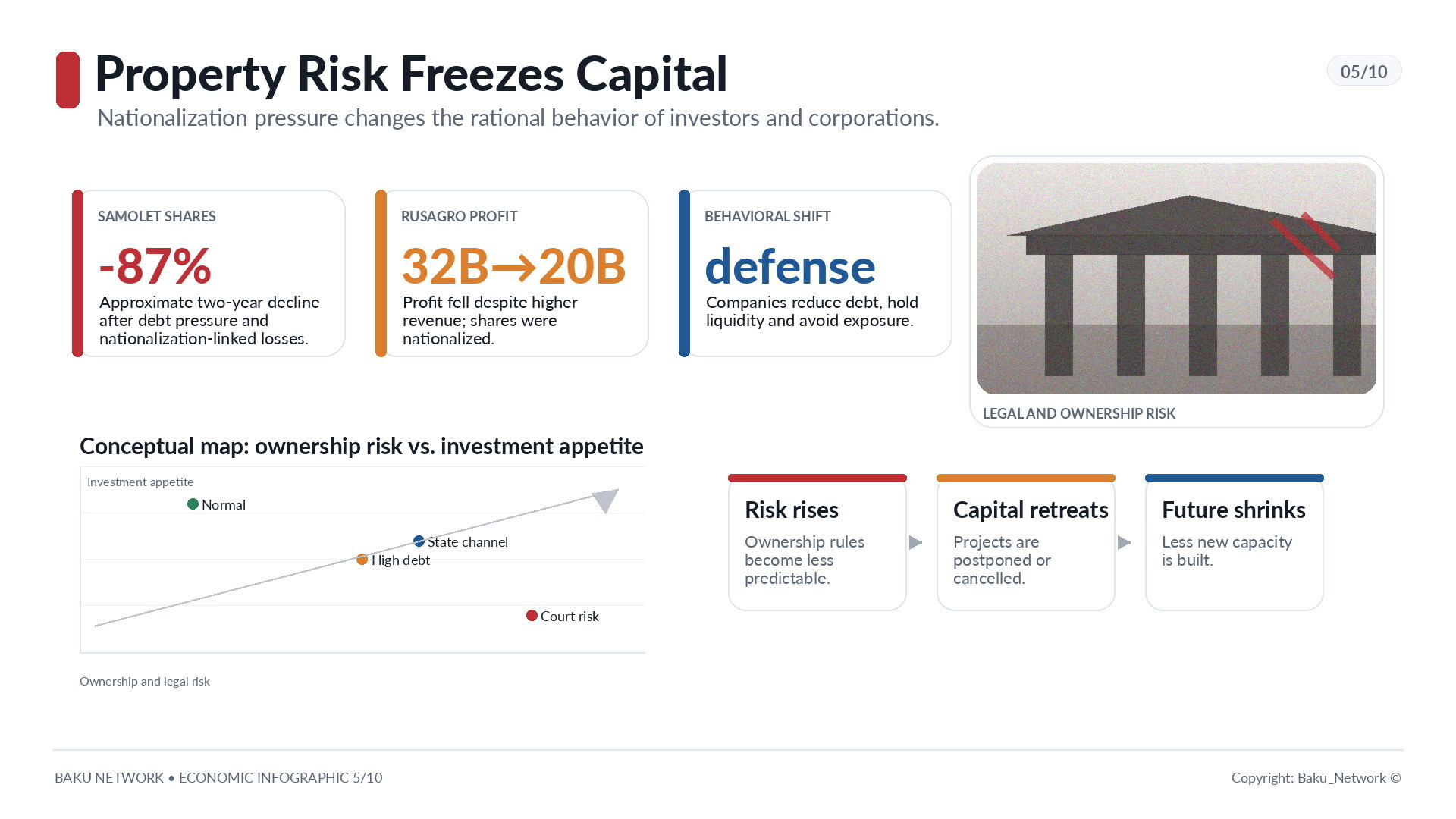

The risk of nationalization is not an abstraction. It has already become part of the business climate. Factories and assets can be seized through lawsuits filed by the Prosecutor General’s Office, while court proceedings can take place behind closed doors. For an investor, this means the main thing: property rights cease to be a reliable basis for long-term planning.

The story of the Samolet Group in the construction sector became a revealing episode. In 2024, the group posted a net profit of 8 billion rubles; in 2025, it recorded a loss of 2 billion. Among the reasons were the cancellation of mass subsidized mortgages, rising debt-servicing costs, and the write-off of investments in the Maryino Quarter project, nationalized by a closed court through a lawsuit filed by the Prosecutor General’s Office. In February 2026, the developer turned to the government for support to reduce its financial burden, and in May it allowed a technical default on its bonds. Over two years, the company’s shares lost about 87 percent of their value.

Another example is Rusagro. The company ranks first in Russia in the production of sunflower oil and mayonnaise, and second in pork and sugar. Revenue in 2025 grew by 18 percent, but profit fell from 32 billion to 20 billion rubles. Rusagro founder Vadim Moshkovich has been under arrest for more than a year, his shares have been nationalized, and the company itself has been transferred to state management.

When such cases occur in systemically important sectors, they become a signal to everyone. One may have a business, assets, employees, investment plans, and financial statements. But one cannot be certain that tomorrow this asset will still be one’s own.

This produces a special type of economic behavior: do not build, do not expand, do not attract attention, do not take on unnecessary obligations, pay down debts, accumulate liquidity. For an individual company, this is rational. For the economy as a whole, it is destructive.

Corporate Statistics Against the Political Showcase

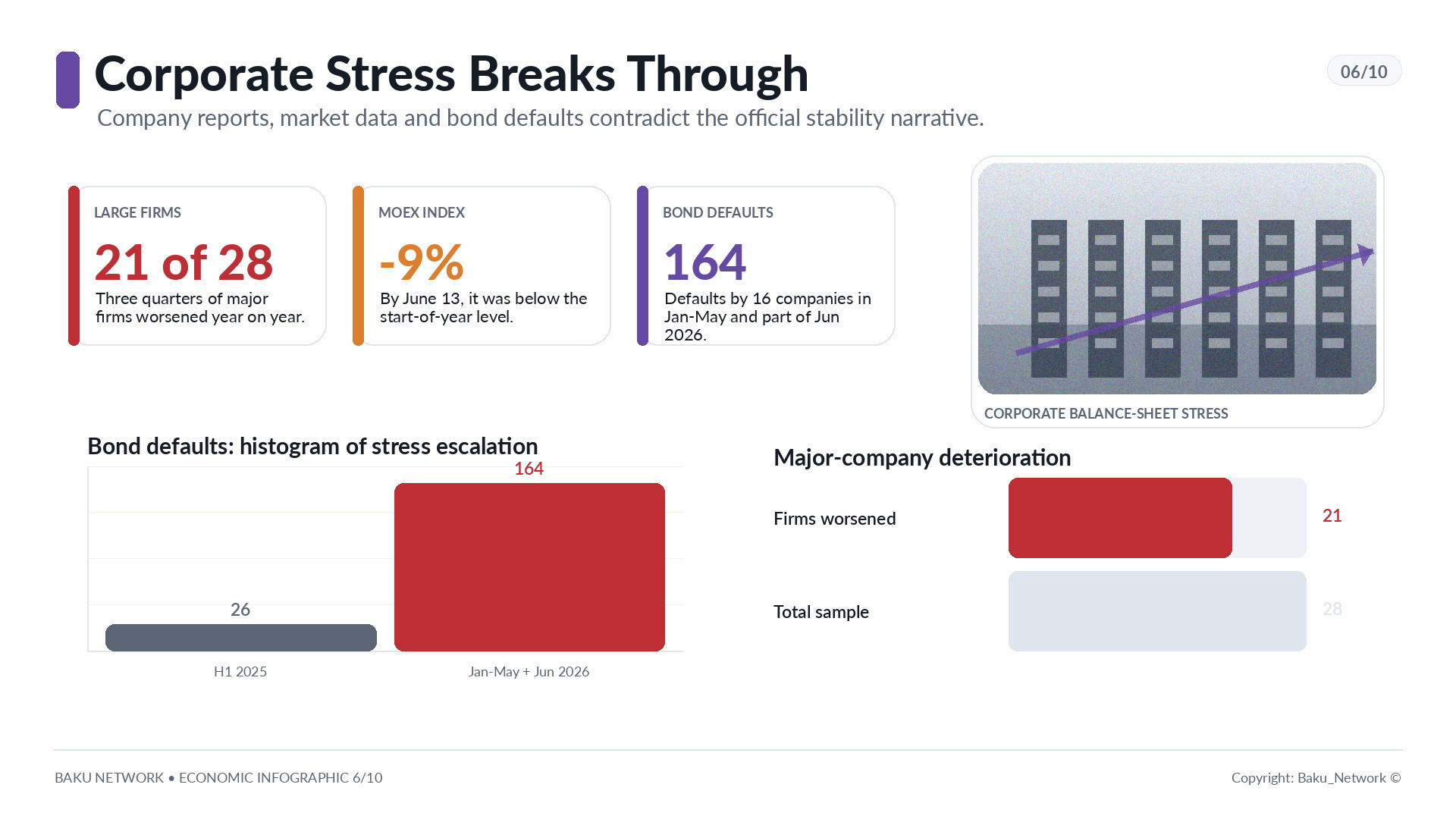

Russian President Putin may say that the Russian economy feels better than Western economies. But corporate reporting speaks another language. According to calculations by Vedomosti, among Russia’s 28 largest companies, the situation worsened over the year for 21. That is three quarters. Small and medium-sized businesses suffered no less: the increase in the tax burden led to a 22.2 percent decline in tax revenues from SMEs in the first quarter of 2026, as the Finance Ministry acknowledged.

By June 13, the Moscow Exchange Index was 9 percent below its level at the start of the year, after a 4 percent decline in 2025. The number of bond defaults rose sharply: in the first half of 2025 there were 26 defaults by three issuers, while in January–May and part of June 2026 there were already 164 defaults by 16 companies, excluding technical defaults.

This is no longer a set of isolated problems. It is a change in the financial climate. Russian corporations are entering an era after windfall profits. Cheap money is gone. Subsidized niches are narrowing. Domestic demand is weakening. Exports are complicated by sanctions, tariffs, logistics, and a strong ruble. Debt is becoming more expensive. Profits are disappearing.

Even retail, which outwardly should benefit from inflation-driven growth in receipts, shows an alarming picture. X5 increased revenue by 19 percent in 2025, but net profit fell by 14 percent. In the first quarter of 2026, profit was already down 27.6 percent year over year. The consumer is shifting to rational consumption: Chizhik is growing by 63 percent, Pyaterochka by 16 percent, and Perekrestok by only 8 percent. This is not a flourishing of consumption, but downtrading, a move into cheaper formats.

Magnit showed an even harsher picture. After buying a controlling stake in Azbuka Vkusa and launching a record investment program, the company ran into expensive debt and weak demand. Operating profit of 70.5 billion rubles was completely consumed by financial expenses, which rose from 24.5 billion to 82.3 billion rubles. The result was a net loss of 16.6 billion rubles after a profit of 50 billion the previous year. Net debt nearly doubled and reached 496 billion rubles; including asset valuation, it exceeded 1 trillion.

When even retail begins to live not on growth but under the weight of debt, it says more about the condition of the consumer than optimistic percentages of retail turnover.

Banks Are Winning While Industry Pays the Price

The only sector that appears relatively healthy is banking. Even there, however, the picture is uneven. Sber increased its net profit by 8 percent in 2025 and by another 17 percent in the first quarter of 2026. Its margin expanded because interest expenses declined faster than interest income. The bank continues to attract household deposits while lending to the corporate sector. Individuals hold 34 trillion rubles in deposits at Sber, while their debt to the bank stands at 20 trillion rubles, two-thirds of which consists of mortgages. Corporations show the opposite ratio: they keep 16 trillion rubles on deposit while owing the bank 32 trillion in loans.

VTB is in a weaker position. Its net profit fell by 9 percent in 2025 and by another 7 percent in the first quarter of 2026. Sber's net interest margin exceeded 6 percent, while VTB's stood at 2.5 percent. Sber's operating expenses amounted to 27 percent of revenue, compared with 39 percent for VTB. Even the banking sector is divided between institutions capable of profiting from expensive money and those whose own cost structures prevent them from taking advantage of the situation.

The greatest paradox, however, lies elsewhere. What benefits banks is suffocating the productive economy. High interest rates support financial margins while destroying the investment logic of manufacturing, construction, retail, agriculture, the automotive industry, and metallurgy.

Infrastructure Is No Longer Building the Future. It Is Repairing the Past

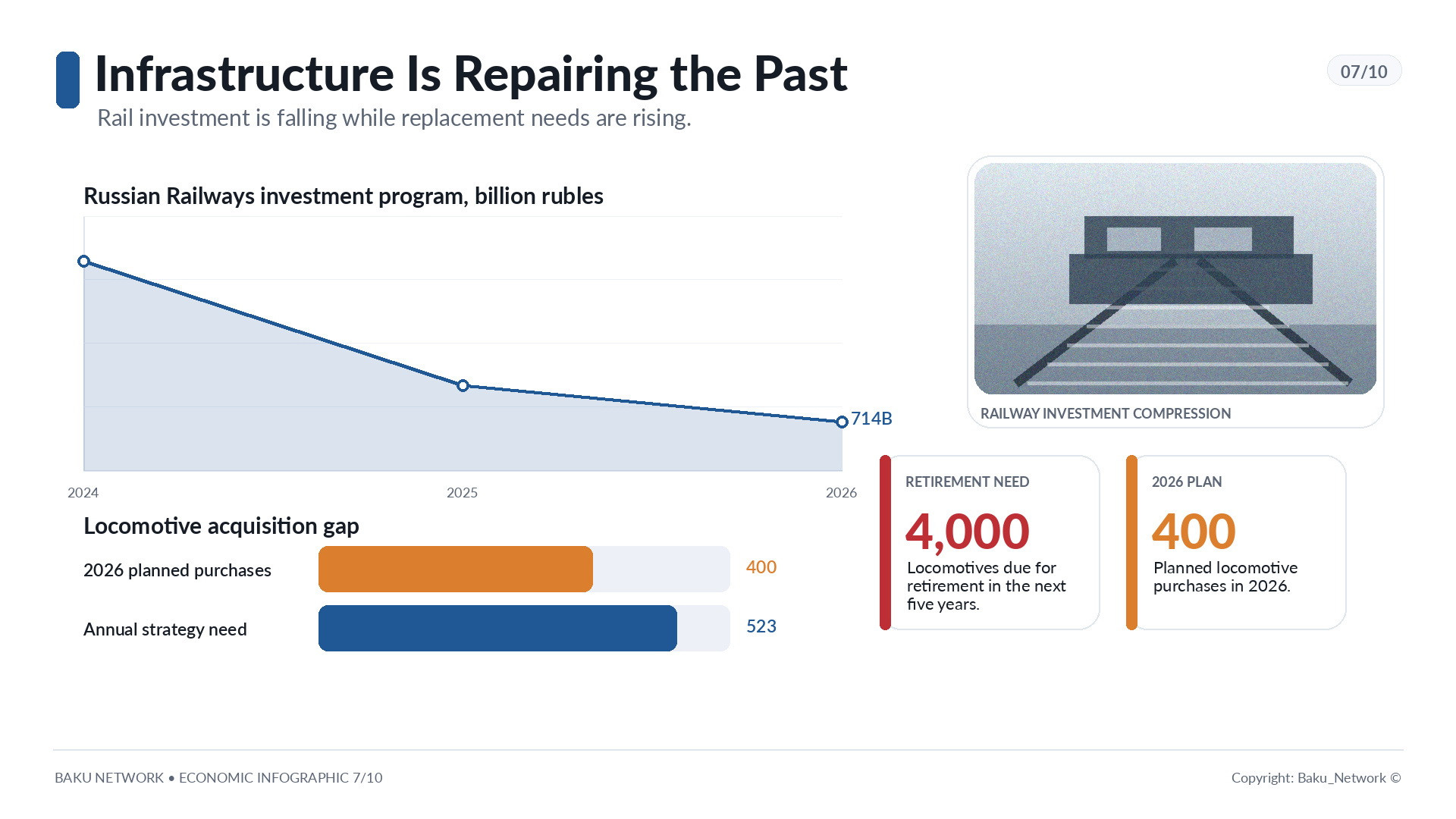

Russian Railways is one of the most important indicators of the country's infrastructure economy. In 2024, the company's investment program amounted to 1.5 trillion rubles. In 2025, it was reduced to 891 billion. In 2026, it was cut by another 20 percent, to 714 billion rubles. Two-thirds of these funds will be spent on maintaining existing assets and ensuring transportation safety.

Only 162 billion rubles remain for new rolling stock. With that amount, Russian Railways plans to purchase 400 locomotives, although the same number cost 260 billion rubles in 2025. Transmashholding has already indicated that it cannot deliver them within the new budget. The problem is especially acute because Russian Railways purchased approximately 2,500 locomotives over the past five years, while 4,000 are scheduled for retirement during the next five years. That leaves a shortfall of about 1,500 locomotives. To fulfill the national transportation strategy, 523 new locomotives are needed every year. Yet the carrier's net profit declined twenty-twofold in 2025.

This is more than railroad accounting. It is a question of the country's transportation connectivity, logistics, exports, regional development, and industrial cooperation. When infrastructure begins spending money primarily on preserving existing assets, the future is postponed.

The Lena Bridge has become a symbol of that postponed ambition. The project has been under discussion since 1985. Yakutsk remains the only one of Russia's one hundred largest cities and regional administrative centers without year-round ground access to the federal highway network. The bridge has repeatedly appeared in national development programs for the Russian Far East and in federal road construction plans. Its estimated cost initially stood at 83 billion rubles, later rose to 176 billion, and was subsequently revised downward to approximately 130 billion. Construction began in 2024 but is progressing slowly. Local media directly link the prospects for completion to a future shift in government priorities away from defense needs and toward civilian sectors.

Projects like this do not die overnight. They simply become permanent promises.

Automobiles, Steel, and Food Processing: The Crisis Is Becoming Sector-Wide

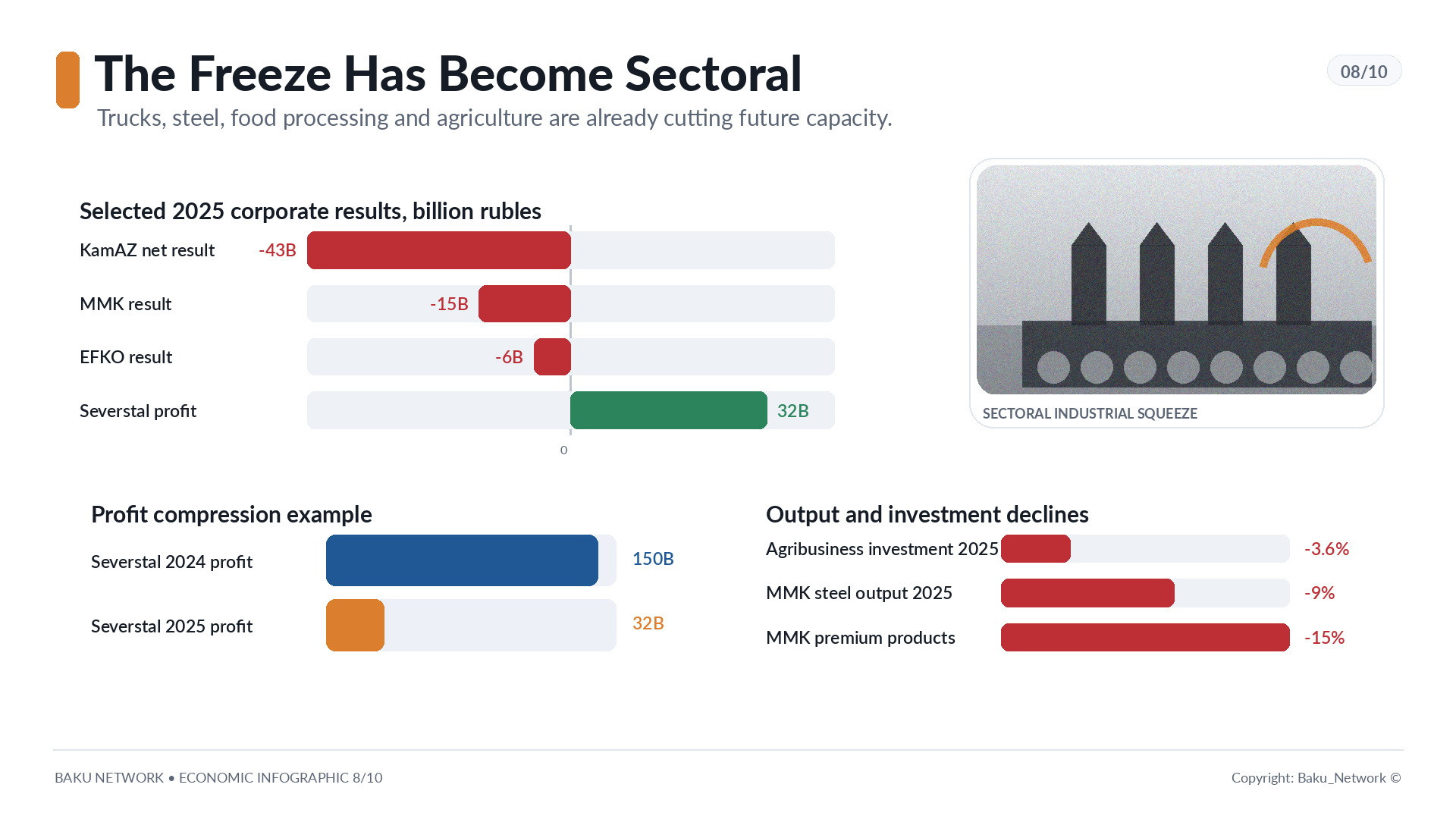

KamAZ has reduced its investment budget by nearly threefold. The reasons are mounting debt and the crisis in the heavy truck market. Chief Executive Officer Sergey Kogogin summarized the devastating arithmetic: in 2022, the K5 long-haul tractor sold for 10 to 11 million rubles. Today it sells for 7.5 million, despite sharply rising production costs. KamAZ reported a net loss of 43 billion rubles in 2025. Interest expenses alone amount to roughly 10 billion rubles per quarter. The company has suspended part of its long-term research and development programs, preserving funding only for the K5 platform and the maintenance of equipment, buildings, and facilities.

This is almost a textbook example of investment degradation: first the distant future is sacrificed, then modernization, then development, until only repairs remain.

The steel industry is displaying similar dynamics. MMK reduced steel production by 9 percent in 2025, sales of steel products by 7 percent, and premium products by 15 percent. Revenue fell by almost 21 percent. Instead of earning a profit of 80 billion rubles, the company posted a loss of approximately 15 billion. Losses continued during the first quarter of 2026. The company attributes the downturn to slowing business activity and deteriorating conditions in the domestic steel market.

Severstal remained profitable, but its earnings shrank almost fivefold, from 150 billion rubles to 32 billion. During the first quarter of 2026, net profit virtually disappeared, falling to just 57 million rubles from 21 billion a year earlier. Investment had to be reduced by 34 percent, while cash holdings declined from 38 billion to 5 billion rubles in a single quarter. The company cites falling prices, declining demand for large-diameter pipes, and the overall contraction of the domestic market.

The food industry is also losing stability. Efko reported its first loss in company history, approximately 6 billion rubles, compared with a profit of 7 billion the previous year. The company openly identifies the reasons: export duties, a stronger ruble, logistical restrictions on the rail route to the Port of Taman, and expensive borrowing. Interest expenses increased by 14 billion rubles, precisely the amount that reversed the company's financial result.

Investment in fixed capital within the agricultural sector declined by 3.6 percent in 2025. In March 2025, there were 2,100 investment projects in agriculture and food processing worth 4.3 trillion rubles. One year later, only 1,500 projects remained, with a combined value of 4.1 trillion rubles. Miratorg cut its investment spending in half, reducing it to 10 billion rubles. Viktor Linnik described the situation calmly, but the meaning was unmistakable: not a single existing project had been canceled, yet no new major projects had been launched.

That is what an investment winter looks like in practice. It rarely arrives as a catastrophe. More often, it takes the form of a simple statement: we are not launching any new major projects.

Technological Backwardness Is Becoming Irreversible

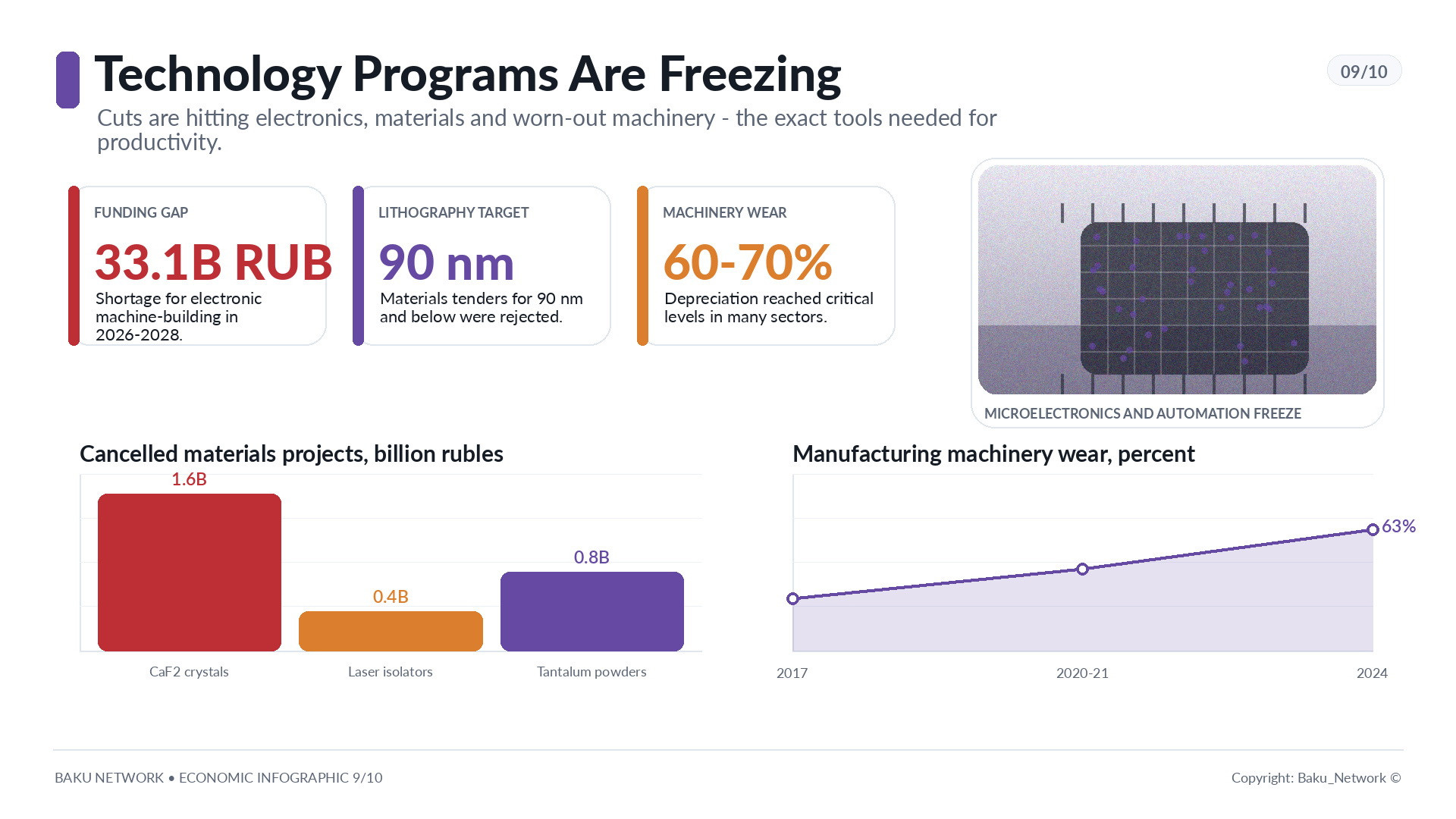

The collapse in high-technology projects is particularly alarming. At the end of 2025, the Ministry of Industry and Trade rejected several tenders related to materials for lithography systems with process nodes of 90 nanometers and below. These projects involved equipment that is critical for Russia's domestic microelectronics industry. Canceled initiatives included pilot production of calcium fluoride crystals for ultraviolet photolithography worth 1.6 billion rubles, laser optical isolator crystals worth 400 million rubles, and tantalum powder manufacturing technology worth 800 million rubles.

Sources attribute these cancellations to budget shortages. The electronic machinery development program lacks 33.1 billion rubles for the 2026-2028 period. Funding is being redirected toward projects considered more urgent. In today's Russia, the word "priority" increasingly refers not to technological advancement, but to immediate political and defense needs.

The Institute for Complex Strategic Studies previously raised an important question: was there ever an investment boom in the first place? Investment increased between 2021 and 2024, yet the commissioning of new fixed assets failed to rise proportionally. In comparable prices, new fixed assets commissioned declined by 9 percent in 2023 and another 4.3 percent in 2024. Over five years, commissioned assets increased by only 11.8 percent, while fixed capital investment expanded by 34.7 percent. Such a gap has never before appeared in modern Russian history.

This means that money was spent, but little new productive capacity was actually created. A significant share of investment flowed into prolonged construction projects, reconstruction, security measures, maintenance of aging assets, and dual-use facilities. Instead of purchasing machine tools, enterprises increasingly buy air defense systems, protective equipment, security infrastructure, and solutions related to military and quasi-military risks. Formally, these expenditures qualify as investment. Economically, they do not increase productivity.

Against this backdrop, equipment depreciation is becoming a strategic threat. According to the latest published data from Rosstat, fully depreciated fixed assets accounted for 22 percent of the economy in 2021. Nearly one in every five fixed assets had an accounting value approaching zero. The situation is even worse for machinery and equipment: the share of fully depreciated machinery increased from 27 percent in 2017 to 30 percent in 2020-2021. Between 2017 and 2024, the wear rate of machinery and equipment in most sectors reached 60 to 70 percent. In manufacturing, it increased from 57.7 percent to 63 percent.

An economy can tolerate aging equipment for years. Eventually, however, obsolete machinery ceases to be an asset and becomes a trap.

Productivity Depends on People, Not Technology

Labor shortages are making the problem even worse. An unemployment rate of 2.2 percent looks impressive in a political report, but for industry it means a shortage of workers. Official estimates place the deficit at approximately 1.5 million people. The Russian Union of Industrialists and Entrepreneurs projects that by the end of the decade it could reach 3 million.

Under conditions of low robotization, this becomes critical. Investment projects require more than financing. They require implementation. Engineers, builders, technologists, skilled workers, designers, and managers are all needed. If the people are not available, even accessible financing cannot be transformed into productive capacity.

Labor productivity in large and medium-sized companies increased by 1.7 percent during the first quarter of 2026 after declining by 0.5 percent in 2025. Yet the broader picture suggests that this improvement resulted not from technological modernization, but from placing greater pressure on the remaining workforce through overtime, labor intensification, and the exhaustion of existing reserves. Real wages continue to grow faster than productivity, creating additional inflationary pressure. Without new investment in equipment, automation, and technology, the ceiling for such growth will soon be reached.

A country that compensates for a shortage of machinery by working people harder is not modernizing. It is simply wearing out both its machines and its workforce more quickly.

A Historical Crossroads: Japan, South Korea, China, and Russia in the 1990s

History has already demonstrated that investment is not merely another statistical indicator. It determines the destiny of an economy.

After the collapse of its financial bubble in 1992, Japan entered stagnation through investment paralysis. Companies cleaned up their balance sheets, paid down debt, postponed expansion, and stopped renewing their productive base. Between 1995 and 2002, average annual real GDP growth amounted to only 1.14 percent, less than one-third of the pace recorded between 1980 and 1991. The "Lost Decade" gradually became the "Lost Twenty Years," and eventually the "Lost Thirty Years."

South Korea followed the opposite path. In 1960, it was one of the poorest countries in the world, with per capita GDP of roughly 79 dollars. After Park Chung-hee came to power in 1961, the government made industrialization and capital investment its central strategy. Export revenues increased from 100 million dollars in November 1964 to 10 billion in 1977. The investment rate rose from 8.6 percent of GDP in 1960 to 29 percent by 1988. GDP expanded by an average of 8.4 percent during the 1960s, 9 percent during the 1970s, and 9.7 percent during the 1980s. By 1995, exports had surpassed 100 billion dollars.

China pursued the same strategy for decades. Between 1981 and 2017, investment in fixed assets grew by an average of 20 percent annually. The investment share of GDP increased from 16 percent in 1960 to 46 percent in 2011. In 2025, China's GDP expanded by 5 percent, reaching 140 trillion yuan. The Chinese model certainly carries debt risks and diminishing returns on capital, but its fundamental lesson remains unmistakable: sustained investment creates industrial power.

Russia has already experienced the opposite scenario. During the 1990s, fixed capital investment collapsed from 51 percent of its 1990 level to just 21 percent by 1998. Even by 2018, in comparable prices, it had recovered to only 52.2 percent of the 1990 level. Privatization failed to generate a meaningful wave of investment. Enterprises consumed the productive capacity inherited from the Soviet period without creating new capacity to replace it.

Today, Russia risks repeating neither Japan's experience in its pure form nor its own 1990s exactly. Yet the underlying logic is remarkably similar: investment declines first, productive assets age next, productivity falls afterward, and eventually the economy loses its ability to renew itself.

Why Investment May Never Return

The official explanation sounds far more reassuring: a high base effect from previous years, an expected correction, a temporary pause. The Ministry of Economic Development notes that capital investment grew by nearly 40 percent between 2021 and 2024, while the first quarter accounts for only about 16 percent of annual investment. Maxim Oreshkin described the decline as "very bad" but likewise attributed it to the high-base effect. Maxim Reshetnikov characterized 2026 as a pause in investment growth.

That argument should not be dismissed entirely. The high-base effect does matter. But it does not explain the full picture. At the same time, businesses are facing expensive credit, the VAT increase from 20 percent to 22 percent beginning January 1, 2026, reduced fiscal stimulus, sanctions, labor shortages, heavier tax pressure, shrinking profits, rising defaults, nationalization, and growing uncertainty about the future.

The share of government funding in fixed capital investment reached 20.5 percent in 2022 but declined to 15.2 percent by the end of 2025 and fell to just 10 percent in the first quarter of 2026. Meanwhile, the share financed from companies' own resources increased from 53 percent in 2022 to 63 percent in 2026. The share of bank financing rose from 10 percent to 14 percent. In other words, investment is increasingly being carried out only by companies with sufficient profits, accumulated reserves, preferential financing, or privileged access to state support mechanisms.

Yet the number of such players continues to shrink. According to the Institute of Economic Forecasting of the Russian Academy of Sciences, industrial enterprises' investment plans remained in pessimistic territory in May, at negative 13 points. The Ministry of Economic Development has already revised its forecast for this year's investment decline from negative 0.5 percent to negative 1.5 percent. The Institute for Complex Strategic Studies believes the downturn could prove even deeper than official projections suggest. Alexander Shokhin has argued that sensitive sectors, including digital technologies and robotics, are not merely being postponed but are being placed into what he described as "deep shock freezing."

That phrase is significant. Digitalization and robotics were supposed to compensate for labor shortages, technological isolation, and aging productive assets. If those sectors are being frozen, then it is not only today's projects that are being suspended. The opportunity to escape the trap is being frozen as well.

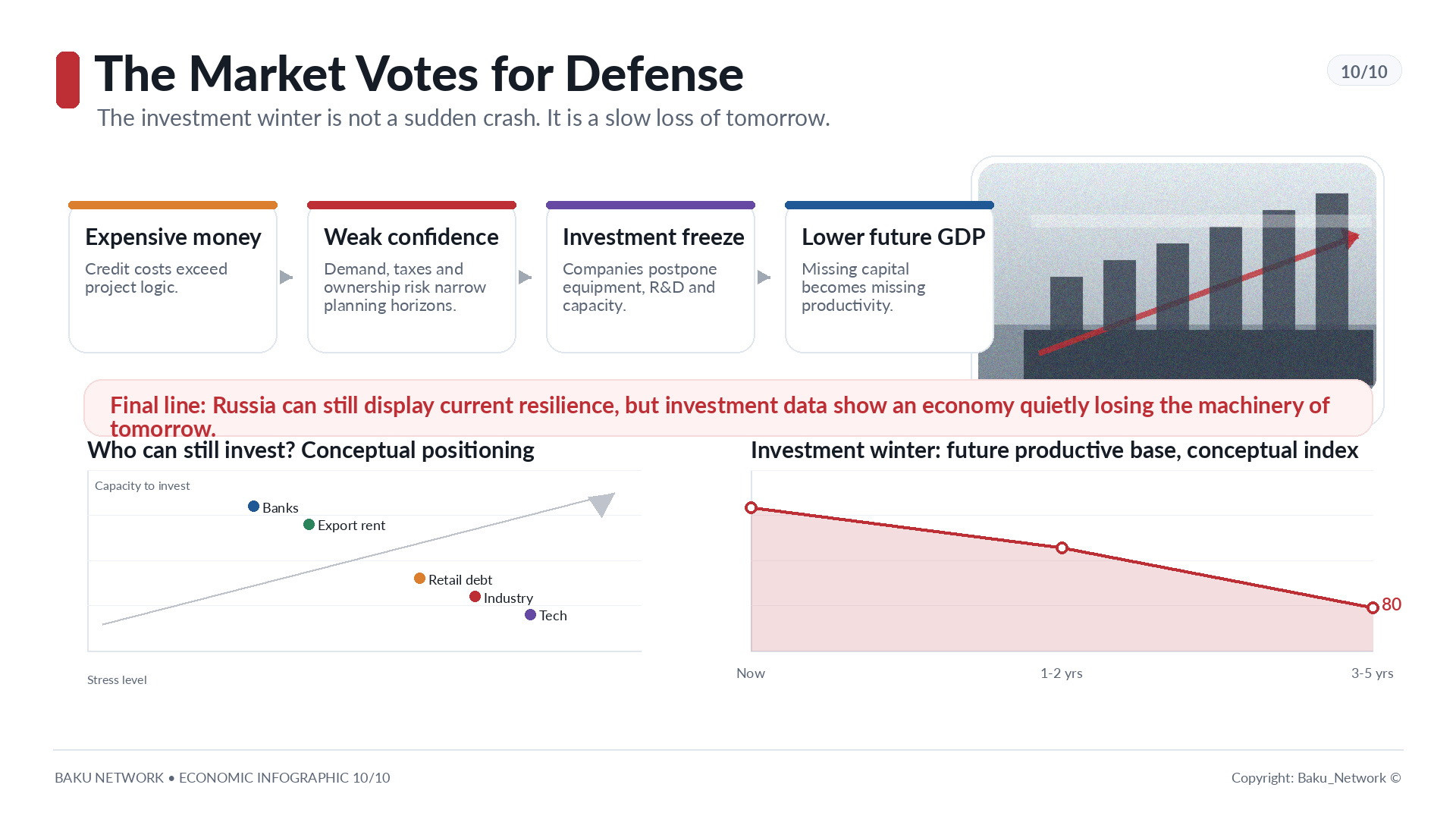

The State Demands Optimism While the Market Chooses Defense

Russian business now faces a painful dilemma. If companies embrace the government's optimism and continue investing despite expensive credit, weak demand, and uncertain rules, they risk losses, default, and dependence on state assistance. If they choose caution, reduce capital expenditures, repay debt, and accumulate liquidity, they behave rationally but may provoke frustration from a government that needs growth, employment, infrastructure, and visible signs of resilience.

This is how an economy of enforced optimism emerges. For businesses, the danger lies not only in making the wrong investment decision but also in openly demonstrating a lack of confidence in the future. Yet markets cannot be ordered to believe. Investment requires more than slogans. It requires affordable capital, secure property rights, access to technology, predictable taxation, stable demand, and confidence in institutions.

Instead, businesses see something very different: expensive borrowing, a strong ruble, higher taxes, sanctions, labor shortages, declining profits, rising defaults, aging productive assets, and the growing risk of nationalization.

In such an environment, the survivors are exporters with manageable debt, companies benefiting from resource rents, banks with strong customer franchises, and a limited number of corporations capable of capitalizing on favorable global commodity markets. Sber, Polyus, Nornickel, and PepsiCo's Russian operations remain among the rare companies still increasing profits. But they do not change the broader picture. An economy cannot be built solely on banks, gold, nickel, and consumer food brands.

Most industries are already operating according to a defensive strategy: avoid risk, avoid expansion, reduce investment, repay debt, preserve cash, and wait. For an individual company, this is a rational response. For an entire country, it is a path toward slow contraction.

A Conclusion Without Illusions

An investment winter does not arrive like a sudden storm. It begins quietly. First, a company postpones construction of a new production facility. Then it cuts research and development. Then it delays equipment purchases. Eventually, only maintenance remains. Finally, aging assets are retired without replacement. In financial reports, these decisions appear under harmless phrases such as "temporary pause," "adjustment," "program review," or "capital expenditure optimization." In reality, they represent the gradual loss of the future.

Russia's economy is not collapsing overnight. In many ways, the situation is more dangerous. It is adapting to its own gradual contraction. It is learning to function without affordable credit, without Western technology, without the extraordinary export revenues of the past, without confidence in property rights, and without a normal planning horizon. But adaptation comes at a price. The longer the country relies on aging productive assets, the fewer opportunities remain for a new wave of growth.

Within a few years, today's decisions will become visible in steel, concrete, railroads, machine tools, locomotives, farmland, factories, microelectronics, and labor productivity. Where nothing was built, nothing will appear. Where equipment was never purchased, nothing will be available to produce with. Where technology was frozen, technological backwardness will become permanent. Where business has been taught to fear the future, it will eventually stop creating it.

That is why today's investment decline is more than an economic headline. It is a political diagnosis. The state may continue for years to present statistics showing stability, maintain employment, redistribute resources, attribute setbacks to the high-base effect, and describe the slowdown as temporary. Investment, however, cannot be deceived. It always reveals where official rhetoric ends and genuine confidence in tomorrow begins.

Today, Russian business is voting not for expansion, but for defense. Not for growth, but for survival. Not for the future, but for preserving what remains of the present.

That is the true meaning of an investment winter. It freezes more than projects. It freezes a nation's historical momentum. Even while the political showcase continues to shine with encouraging growth statistics, beneath it an economy may already have quietly stopped building its own tomorrow.